Buying in San Francisco means learning how to write a strong offer without taking on unnecessary risk. Contingencies are your safety net, but they also influence how a seller reads your offer. If you understand what each contingency does, how timelines work, and how neighborhood dynamics change the strategy, you can compete with confidence. This guide breaks down the essentials so you can protect your deposit and still put your best foot forward. Let’s dive in.

What contingencies are

A contingency is a condition in your contract that must be met for the sale to proceed. If the condition is not met within the agreed window, you can cancel and keep your earnest money, or ask the seller to address the issue.

In San Francisco, you will most often see these categories:

- Loan/financing

- Appraisal

- Inspection (general, systems, roof, foundation)

- Pest/termite (WDO)

- HOA/condo document review

- Title

- Sale of your current home

- As‑is or limited‑repair terms

With these tools, you can request repairs or credits, renegotiate price, or cancel and keep your deposit when conditions are not satisfied.

The key protections to know

Financing and appraisal

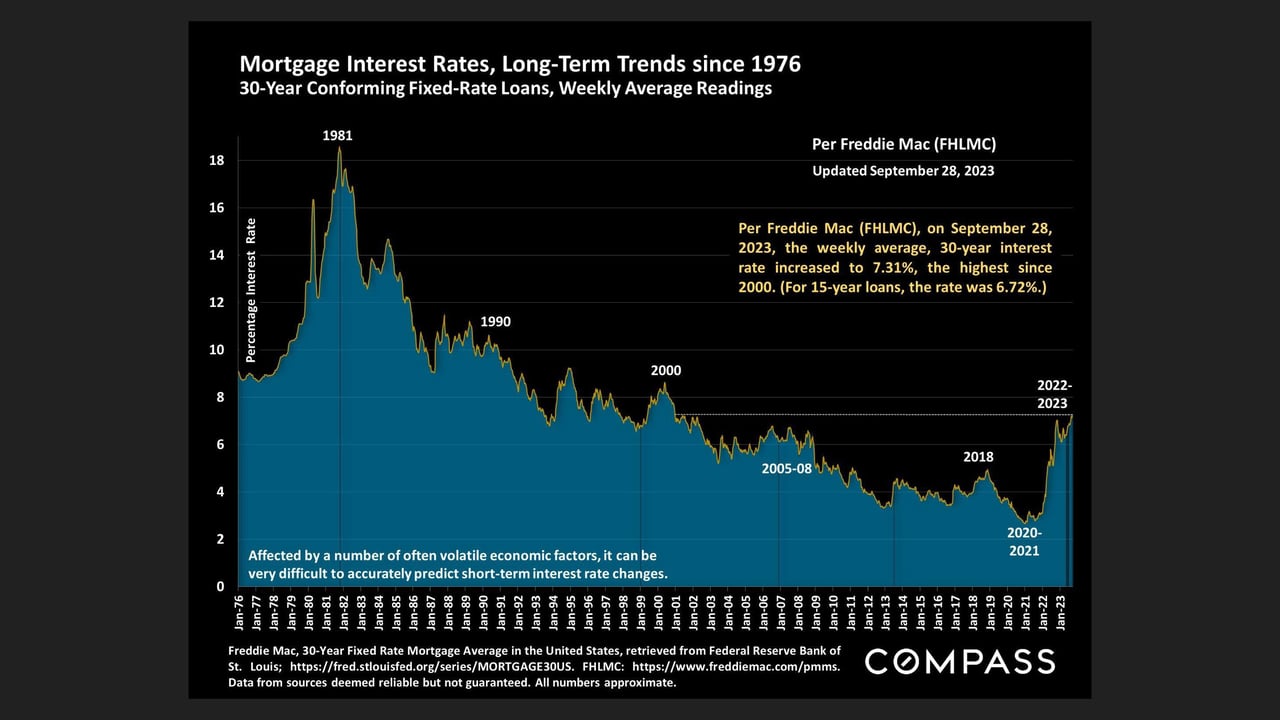

A financing contingency gives you time to secure loan approval. An appraisal contingency addresses the risk that a lender’s valuation comes in below your contract price. In many San Francisco deals, the appraisal timeline runs alongside the loan process.

Some competitive offers include an appraisal gap clause. This means you agree to cover a set amount if the appraisal is short. It can strengthen your offer but does not remove lender requirements.

Inspection and pest

An inspection contingency lets you investigate property condition. In older SF homes, buyers focus on structure, roof, water intrusion, systems, and foundation. A separate pest or WDO contingency targets termites and wood‑destroying organisms that are common in timber structures.

You can request repairs or a credit, or cancel if major issues appear and the seller will not address them. If you use “information‑only” language, you still inspect but limit repair asks, which can appeal to sellers when competition is high.

Title and HOA/condo docs

A title contingency protects you if there are problems with ownership records or unacceptable title exceptions. For condos and co‑ops, an HOA document review contingency lets you examine CC&Rs, budgets, reserves, meeting minutes, and any pending special assessments.

California gives narrow rescission rights for HOA documents after they are delivered. Plan review time into your offer so you do not miss those windows.

Sale of your current home and as‑is terms

A sale contingency makes your purchase dependent on selling another property. In hot SF pockets, this is rarely accepted. As‑is terms limit repair obligations, but they do not prevent you from inspecting. You still want to understand the building and any future costs.

How timelines and escrow work

Most conventional escrows in San Francisco run about 30 to 45 days. Cash can close faster when title and funding are straightforward.

Common practice timelines include:

- Inspection: 7 to 17 days from acceptance

- Loan: 17 to 21 days to secure commitment

- Appraisal: typically completed 7 to 14 days after it is ordered

- HOA document review: often 3 to 5 business days after delivery

In competitive situations, buyers sometimes shorten inspection to 7 days and tighten appraisal or financing to about 10 to 14 days. Only choose shorter windows if your lender and inspectors can perform on time.

When you remove a contingency, you sign a form that commits you to proceed. If you later cancel for a reason not allowed by the contract, you risk losing your earnest money. Your deposit is held in escrow and can be staged, with a larger amount posted after contingency removal to show commitment.

San Francisco disclosures and local focus areas

State and federal disclosures to expect

California requires a Transfer Disclosure Statement and a Natural Hazard Disclosure, among other notices. Federal rules require a lead‑based paint disclosure for homes built before 1978. Review these early and track delivery dates so your rights are preserved.

Local SF items to confirm early

San Francisco has unique conditions and programs that matter for due diligence:

- Soft‑story and seismic retrofit status for certain multi‑unit buildings

- Rent control and tenant protections for occupied properties

- Historic district or landmark restrictions that affect exterior changes

- Building condition priorities: older foundations, chimney stability, roof life, water intrusion, mold, and aging mechanicals

- Sewer lateral condition and any municipal notices

- Seismic hazard and fault zone disclosures

- For condos: HOA reserves, upcoming capital projects, insurance, and special assessment risk

These topics can change cost of ownership and project timelines, so bring them into your review from day one.

Strategy by neighborhood competitiveness

San Francisco is a city of micro‑markets. Your contingency strategy should match the property and the neighborhood.

Hot micro‑markets

In the Marina, Pacific Heights, and some North of Panhandle offerings, multiple offers are common. Sellers often prefer shorter inspection periods, minimal contingencies, and stronger deposits.

To compete, buyers often:

- Get full lender pre‑approval before writing

- Complete pre‑offer inspections when possible

- Shorten, but do not recklessly waive, key contingencies

- Offer capped appraisal gap coverage if finances allow

In‑demand but variable areas

NoPa, Hayes Valley, and the Inner Sunset can be very competitive for turnkey homes, though properties needing work may allow more negotiation. Align your timelines with the home’s condition and the buyer pool you face that week.

Slower or more balanced submarkets

In parts of the Outer Richmond, Outer Sunset, Bayview, and the Excelsior, market times are often longer and bidding can be less intense. You can usually keep standard contingency windows and make thoughtful repair requests without losing the deal.

Multi‑unit and investment listings

Investment buyers often accept limited inspection periods or as‑is structures, especially when opportunity is priced in. Pay extra attention to retrofit compliance, tenancy status, and income documentation.

Balance strength with protection

Use these steps to keep your offer sharp and your risk measured:

- Get a robust lender pre‑approval, including underwriting of income and assets.

- Discuss pre‑offer inspections where access is feasible.

- Set staged deposits: a reasonable initial amount, then a larger deposit after contingency removal.

- Maintain cash reserves to cover an appraisal gap or urgent repairs.

To make terms seller‑friendly while limiting exposure:

- Shorten the inspection period but keep the right to cancel for defined major issues.

- Use clear appraisal gap language with a dollar cap you can actually fund.

- Consider information‑only inspections to learn about the property while easing repair demands.

Avoid common pitfalls:

- Do not remove contingencies without understanding deposit risk and lender conditions.

- Be explicit about what is as‑is versus subject to requests.

- Track all disclosure and HOA document delivery dates and respond within the contract timelines.

Understand the consequences:

- If you waive or remove a contingency, then cancel without a contract reason, your deposit may be at risk.

- A lender can still deny a loan if the appraisal is too low. If you waived appraisal, you may need to bring cash or face breach exposure.

Choosing your path

The right mix of contingencies depends on your comfort with risk, your cash position, the property’s condition, and local demand at that price point. If you are light on reserves, keep protections and consider shorter but realistic windows. If you have more liquidity, you can offer limited appraisal gap coverage and a tighter inspection period while still protecting your deposit.

For condos, prioritize HOA documents, reserves, and special assessment exposure. For older single‑family homes, elevate structure, foundation, and water management in your inspection plan. Align your approach with the micro‑market realities on that block, not just the citywide headlines.

Next steps

If you want an offer strategy that matches the property, the neighborhood, and your risk tolerance, connect for a focused plan. From pre‑offer prep and inspections to calibrated timelines and negotiation, you will have clarity at every step. Start the conversation with Brandi Mayo.

FAQs

What is a contingency in a home offer?

- A contingency is a condition that must be satisfied for the sale to proceed, giving you the right to cancel and keep your earnest money if it is not met in time.

How long are typical SF contingencies?

- Common timelines are 7 to 17 days for inspections, 17 to 21 days for loan approval, and 7 to 14 days for appraisal, with HOA review often 3 to 5 business days after delivery.

Should I waive the inspection contingency in a bidding war?

- You can, but it increases risk. Consider a pre‑offer inspection or a shortened inspection window so you still have a path out if major issues surface.

What if the appraisal comes in low on my SF purchase?

- With an appraisal contingency, you can renegotiate, add cash, or cancel. Without it, a lender may not fund, and you would need to cover the gap or risk breach.

How do micro‑markets affect my terms in San Francisco?

- In hot pockets like the Marina or parts of NoPa, sellers favor shorter timelines and fewer contingencies. In slower areas, standard windows and repair requests are more acceptable.

What SF‑specific disclosures should I review early?

- Confirm seismic retrofit status for applicable buildings, tenancy and rent‑control details, any historic restrictions, sewer lateral condition, and for condos, HOA reserves and special assessments.

What is the difference between removing and waiving contingencies?

- Removing means you sign off during escrow and are then obligated to proceed. Waiving means you never had the protection. Both increase deposit risk if you later cancel without a contract reason.